Two ways to fund growth. They are not interchangeable.

Venture capital and revenue-based financing are both legitimate funding tools. They are built for different situations, different software entrepreneurs, and different definitions of success. The right answer depends on what you are actually building and where you want to end up.

This page is not an argument against VC. Most software entrepreneurs we talk to have had good experiences with their investors. What has shifted is the assumption that equity is the only serious option at the growth stage. It is not.

The alignment question

Every investor says they are aligned with software entrepreneurs. The more useful question is: aligned by what mechanism?

With equity, alignment depends on shared goals and good relationships. That works well when interests overlap. But equity investors have fund timelines, LP expectations, and portfolio dynamics that can pull in a different direction from a software entrepreneur’s long-term vision. The misalignment is not usually bad intent. It is structural.

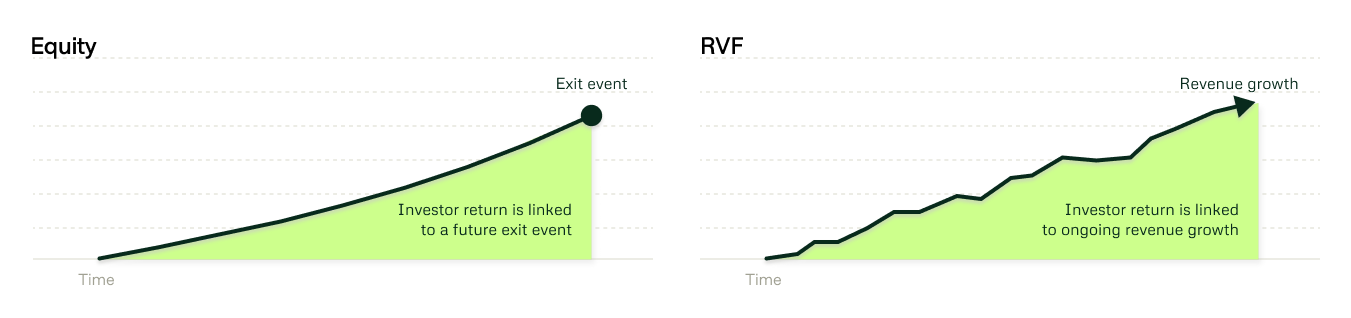

With revenue-based financing, the alignment is mechanical. Round2 Capital’s returns are a percentage of your revenue. We make money when your company grows. There is no scenario where we benefit from pushing you toward an exit that does not work for you. When you do well, we do well. That is it.

What VC is actually optimised for

Venture capital works best when a business needs large capital to capture a market quickly, has a long path to profitability, and is building toward a significant liquidity event.

The structure —high dilution, board involvement, explicit exit orientation is designed for that profile.

If that is the business you are building, VC may well be the right instrument. The capital volumes, the networks, and the validation signal that comes with a top-tier round have real value.

But if you are a software business at EUR5m to EUR25m ARR, growing steadily, with strong margins and no particular desire to run toward an exit on someone else’s timeline — the VC structure may create friction that the business does not need.

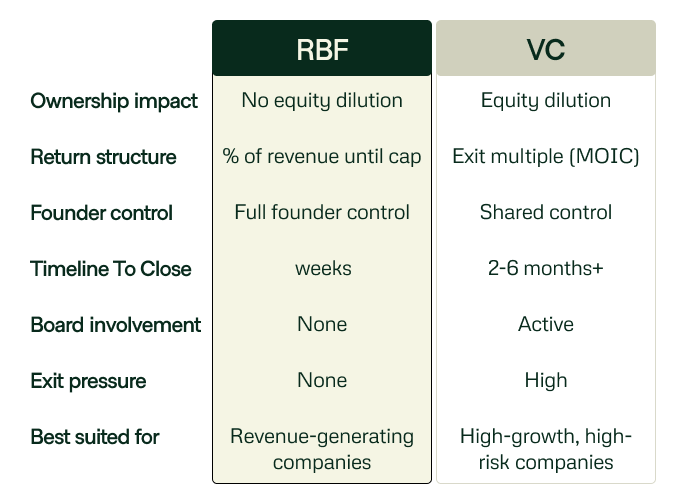

The comparison

The European context

Five years ago, a SaaS company at EUR10m ARR growing 30% would raise a Series B without much debate. The only real question was which VC to take it from.

That market has changed. Deal volume across European growth-stage funding fell 9% across 2025 and the flight to quality has continued into 2026. Investors are backing fewer companies at higher conviction. The bar for a VC round has moved up significantly.

That creates a gap, and it is a real one. A business at EUR8m ARR, growing 25% a year, has a clear path to EUR25m. But that path goes through a financing decision that most of the capital market does not know how to make well. VCs want faster growth. Banks want EBITDA history a growth-stage company has not built yet because it has been reinvesting correctly.

Revenue-based financing exists in that gap