The European software funding market has shifted. Here is what that means.

The conditions that defined software funding from 2019 to 2022 no longer apply. Deal volume has fallen, underwriting assumptions have changed, and the gap between early-stage access to capital and growth-stage access to capital has widened.

This is not a temporary dislocation. It reflects structural changes in both the supply of capital and the risk profiles of the companies seeking it.

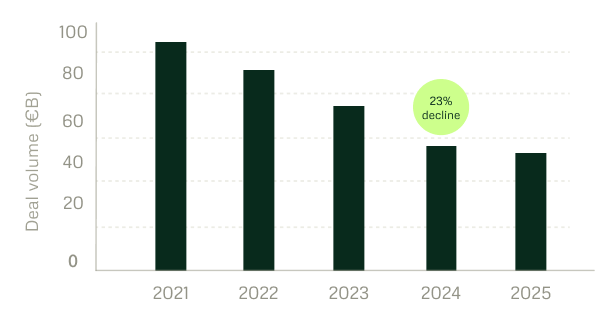

What happened to growth-stage funding

European deal volume fell 9% across 2025. The so-called flight to quality has continued into 2026: investors are writing fewer cheques and concentrating conviction in a smaller number of companies.

The companies in the EUR5m to EUR25m ARR band, growing steadily, with real products and real customers, have felt this most acutely. They are too large for seed-stage capital and too small, or too slow-growing, for the tier of VC that is still actively writing growth cheques. Banks remain difficult for growth-stage software businesses because the EBITDA history they require is often absent in companies that have been reinvesting correctly.

More companies are starting in Europe than at any point before. Fewer are scaling at the speed the underlying business would support. This is often framed as a talent problem or a market maturity issue. In most cases it is a financing problem that has not been named clearly enough.

AI and the predictability question

Recurring software revenue used to be straightforward to underwrite. Churn was manageable, category dynamics were slow-moving, and a company with 5 years of ARR growth had a reasonably predictable next 3 to 5 years.

That calculus is more complicated now. AI-native companies are growing faster — ARR compounds more quickly once the product lands. But AI is also compressing entire software categories: products that took years to build can now be replicated, or replaced by a feature in a larger platform.

Every time Round2 Capital looks at a company — and only 5 to 6 of every 1,000 we see become a deal — the central question is the same: will this revenue actually last? For the wider market, that question has only recently moved to the front of the room; AI made it impossible to ignore. For us, it has been one of the defining questions from the start.

That is why our checklist has never stood still. Over the last 8 years we have looked at more than 8,000 companies and invested in more than 40, refining how we underwrite at every step — and we have been reading AI into that picture for far longer than it has been a public headline. ARR, growth rate, and churn still matter, but they were never the whole answer. The question that has stayed constant is the one that matters most: is the business model generating this revenue still defensible in the next years?

The BDC situation and what it does not mean for European lending

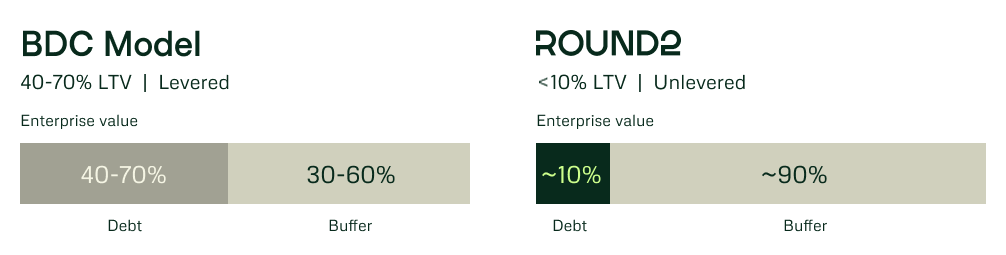

US Business Development Companies scaled their software exposure from around USD 8B in 2015 to over USD 500B by the end of 2025. When AI concerns hit SaaS valuations, software stocks fell sharply and financial media responded with broad category labels — ‘software lending in crisis’, ‘private credit under pressure’.

The label does work it should not. A European lender operating at 10% loan-to-value is not structurally comparable to a US vehicle levered at 6x EBITDA, but in a headline they are both just ‘software lending’. The category travels faster than the analysis.

For context: Round2 Capital caps entry LTV at 10% on every investment; across the portfolio, our actual average is just 4.6%. At that level, a portfolio company would need to lose more than 95% of its enterprise value before Round2’s principal is at risk.

The BDC vehicles facing stress right now financed software buyouts with debt representing 40 to 70% of transaction value. A 30% decline in enterprise value puts those lenders underwater.

These are different instruments, different geographies, and different risk profiles. The challenge is making that distinction legible when the broader narrative is moving fast.

What holds up when conditions turn

Every private credit lender can show you a backtest that looks good: revenue grew, repayments stayed on schedule, losses were minimal. The limitation of a backtest is that it only shows what works in favourable conditions.

The questions that decide an outcome are harder. What happens when average revenue growth drops from 25% to 10%? When a company loses its second-largest customer? When an entire vertical faces sudden pricing pressure from AI competitors within a quarter?

The portfolios under pressure today were built and structured for benign conditions. Fixed-rate repayment that worked at 30% software growth stops working when growth slows and valuations compress — the obligation stays flat while the business behind it does not.

Round2’s repayments are a share of revenue, so they move with the business: when revenue softens, so does the repayment, rather than holding firm at the hardest moment. That is not a feature added once conditions changed — it is the design choice the structure was built on, made with the difficult questions in mind from the start.