You built the business. You should still own it.

At some point, every growth-stage software entrepreneur faces the same question: how do I fund the next phase without giving the company away piece by piece?

For most of the last decade, the answer was assumed to be venture capital. Raise a round, dilute your ownership, take on investors with their own timelines and return expectations, and build toward an exit that works for them as much as it works for you.

That assumption is worth questioning.

What dilution actually costs

The dilution number on a term sheet is easy to understand. What is harder to quantify is everything else that comes with it.

Equity investors have their own timelines. Their funds have lifecycles. Their LPs have expectations. That is not a criticism, it is just how the structure works. But it means that software entrepreneur and investor interests do not always point in the same direction, especially when it comes to timing an exit, deciding whether to optimize for growth or margins, or choosing how fast to scale.

Non-dilutive capital does not carry that dynamic. Round2 Capital’s returns improve when your company grows. There is no incentive to push you toward an outcome that works for us but not for you. When you benefit, we benefit. That is the whole model.

The cost no one talks about: software entrepreneur time

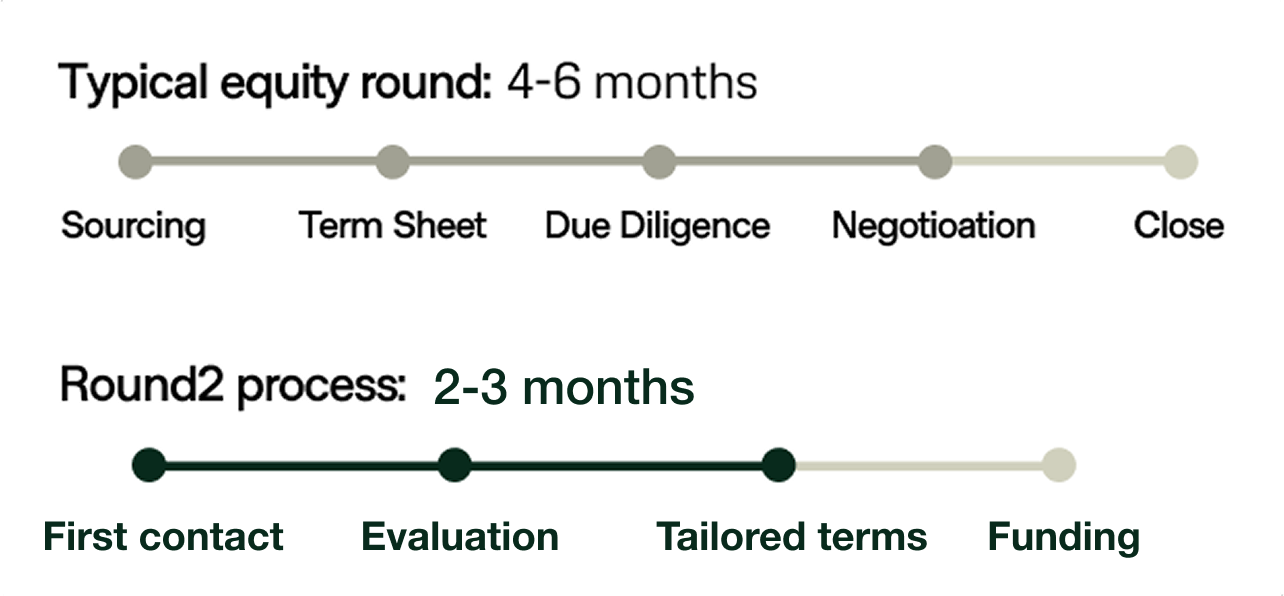

A full fundraise, preparing materials, running a process, managing due diligence, negotiating terms, takes most CEOs six months of serious attention. Those are four to six months when your focus is not on the product, the customers, or the team underneath you.

Deals slip. Hiring slows. Decisions that needed to be made in Q2 get made in Q4. By the time the round closes, the company that comes out is often slightly weaker than the one that went in, not because the raise failed, but because the software entrepreneur’s attention was somewhere else for two quarters.

Round2 Capital’s process closes in weeks. The software entrepreneur does not have to step away from running the company to get the capital.

What non-dilutive capital is not

It is worth being direct about the limits. Non-dilutive financing is not right for every situation.

If a business needs capital to survive rather than to grow, RBF is not the answer. If revenue is not genuinely recurring, if it depends on project wins, service contracts, or one-off implementations, the model does not work. And if the ambition requires a war chest that only a large equity round can provide, that is a legitimate reason to raise equity.

The point is not that equity is wrong. The point is that it should be a choice, not an assumption.

Who qualifies

- B2B Software with at least EUR 3m ARR

- Recurring revenue as the primary revenue model

- Demonstrable growth track record

- Business capable of reaching break-even independently the capital is for acceleration, not survival