We pass on more deals than we close. Here is what we are actually looking for.

We are not the right fit for every software business. The criteria we use are specific, and they exist because revenue-based financing only works when the fundamentals support it. A deal that looks good on the surface but fails on one or two of these criteria is still a pass, regardless of how promising the company looks in other ways.

The following is what we look at, and why each of these things matters to the model.

Minimum EUR3m in annual recurring revenue

This is not an arbitrary threshold. It is the floor below which the RBF model does not generate enough repayment volume to be useful to either side.

Below EUR3m ARR, the financing amount required to move the needle for the business tends to be too small to justify the underwriting process, and the repayment period stretches to a length that creates uncertainty rather than resolving it.

If you are not there yet, that is not a reason not to talk to us. We have directed early-stage companies toward other instruments and had them come back when the numbers were right.

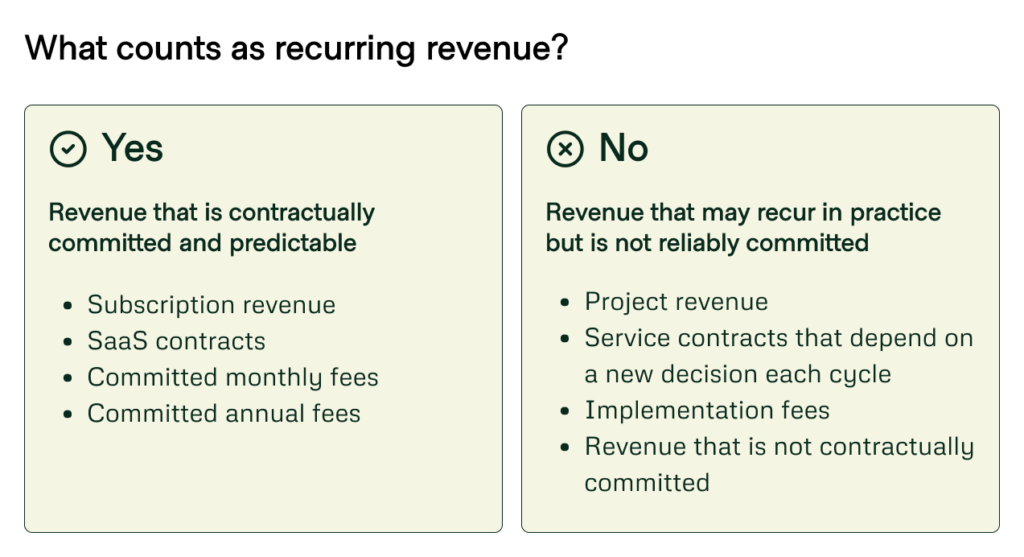

Recurring revenue — genuinely recurring

This is the single most common reason we pass on an otherwise interesting business.

Recurring revenue means subscription revenue, SaaS contracts, and committed monthly or annual fees. It does not mean revenue that recurs in practice but is not contractually committed.

It does not include project revenue, implementation fees, or service contracts that depend on a new decision every cycle.

Our repayments are a fixed percentage of monthly revenue. That model requires predictability. If revenue can drop by 40% in a month because a large project ended, the model breaks. We are not set up to manage that kind of variability, and it would not be good for the portfolio company either.

The business can reach break-even without us

This is a harder one to articulate but it is important. We are not rescue capital. We finance growth, which means the business we are financing needs to have a viable path to break-even on its own if the external environment changes.

If the investment is what is keeping the lights on, there is no growth to accelerate. And if the business cannot survive a period of slower growth without ongoing external capital, the risk profile changes in ways that revenue-based financing is not designed to absorb.

This does not mean you need to be profitable now. It means the model is sound enough that you could get there if you needed to

A demonstrable track record of growth

We look for sustained growth, not a single exceptional quarter. A business that grew 80% last year off a small base and has been flat since does not have the track record we are looking for.

What matters is that the growth is structural, driven by product, by market, by a repeatable sales motion, rather than circumstantial. We want to see that the trajectory has been consistent enough to underwrite a reasonable forward projection.

Technology at the core

We are not generalist lenders. We work with companies where the technology is the business, not a tool the business happens to use. A professional services firm that uses good software internally does not qualify. A software business that happens to have a services component might, depending on how the revenue splits.

The reason is practical: tech-driven businesses have the margin profiles and revenue characteristics that make our model work. Businesses that are primarily delivering services through people have different economics, and those economics are not a good fit for revenue-based financing.

What happens if you don’t qualify today

We will tell you directly. We assess every company on its own terms, and if a business does not fit our criteria we will explain which criteria it does not meet and why.

In some cases, the answer is ‘not yet’. Revenue is growing toward the minimum, or the services revenue is being transitioned to subscription, or the break-even question needs another six months of work. We have financed companies that came back to us after addressing exactly those issues.

In other cases, we are simply not the right instrument, and we will say that too, without wasting your time.